Zar Amrolia gets noticed

XTX Markets, a three-year-old startup, had been named the third-largest market maker in the $5.1 trillion-a-day market, leapfrogging some of the world’s biggest banks including Citigroup Inc. and Deutsche Bank AG. For a company that ranked 12th the previous year, it was a coup.

Now the London-based company, which doesn’t have any human traders, is setting its sights on U.S. markets.

XTX aims to expand in stocks and Treasuries, markets in which it says customers aren’t getting a good deal. “We don’t believe that all markets are fair and efficient,” says Zar Amrolia, XTX’s co-chief executive officer. He points to U.S. equities in particular. “The speed is so high, it’s really providing no benefit to the market at all—it’s detrimental,” he says, adding that it raises costs for investors. Amrolia, who has a doctorate in mathematics from Oxford University, was co-head of fixed income, currencies, and commodities at Deutsche Bank AG before leaving in 2015 and starting XTX with fellow Deutsche Bank alumnus Alex Gerko, who also has a Ph.D. in math.

They’re looking to change the rules of the game. In a letter to the U.S. Securities and Exchange Commission in November, Amrolia and co-CEO Gerko called for a “wholesale rollback” of Regulation NMS—a landmark SEC rule approved in 2005 that accelerated a shift to electronic trading in the U.S. stock market. “The race for speed in trading has reached an inflection point where the marginal cost of gaining an edge over other market participants, now measured in microseconds and nanoseconds, is harming investors,” they wrote.

Their concerns echo those highlighted in Michael Lewis’s 2014 book, Flash Boys: A Wall Street Revolt. In it, Lewis describes how high-frequency traders use complex algorithms to rapidly move in and out of stock positions, making money by arbitraging small price differences and front-running other investors’ trades.

XTX also criticized so-called latency arbitrage in its letter to the SEC, arguing for the introduction of speed bumps to slow trading and enable market makers to post better prices without getting picked off by high-frequency traders. “It is ambitious, but it’s also practical and timely,” says Eric Swanson, the company’s New York-based Americas CEO. He formerly served as general counsel and corporate secretary at exchange operator Bats Global Markets, which was bought by Cboe Global Markets Inc. in 2017.

Although it’s advocating for change, Swanson points out that XTX’s growth plans aren’t contingent on shifting rules. “In U.S. equities, we’re in this for the long haul,” he says. “We realize that the regulatory changes are a long game.”

This isn’t the first time the company has criticized market practices. In currencies, XTX advocated for changes to “last look,” a controversial practice that allows dealers to back out of losing trades.

It’s “absurd” that some market makers still retain the option to hold trades for as long as 200 milliseconds before striking a deal or pulling out, Amrolia says. XTX hasn’t done away with last look entirely, but it removed the holding time between a client’s trade request and its acceptance or denial of the deal.

That change is critical for one of XTX’s clients. Neil McDonald, head of trading and quantitative analytics at retail foreign exchange platform Oanda Corp., says he gets consistently good prices from XTX, which has the lowest rejection rate among the market makers with whom he trades. “I’m very impressed,” he says. XTX is more open about its operations and hungry to win business compared with some banks, which aren’t always attentive to customers, he says.

XTX’s rise comes in the wake of a price-rigging scandal in FX that prompted global banks to pay more than $10 billion in fines and penalties. Three British traders were acquitted in October of fixing prices in a chat room that was called the “Cartel.”

McDonald says XTX has also benefited from starting from nothing to build its electronic trading systems. “They’ve had the advantage of being able to build something from scratch and not try to fix the airplane while it’s flying, which is what the banks are trying to do,” he says.

XTX has 118 staff globally, including 10 people at its New York office in Hudson Yards, Amrolia says. Since he and Gerko founded the company, it’s increased trading volume to an average of $150 billion a day across stocks, currencies, fixed income, and commodities.

XTX’s office in the King’s Cross neighborhood of London is like someone’s fantasy of a tech company headquarters. Bar? Check. Sleeping quarters? Check. There’s also a replica Apollo 11 landing capsule, saunas, arcade games, and a self-playing piano. Staff perks include yoga classes and massages, as well as regular staff events such as a chess tournament in January.

The company made a profit of about £61 million ($80 million) in 2017, little changed from a year earlier, according to the annual report for that year, the latest for which data are available. More recently, its global cash equities volumes jumped 74 percent in 2018 from a year earlier, while FX volumes were up 46 percent.

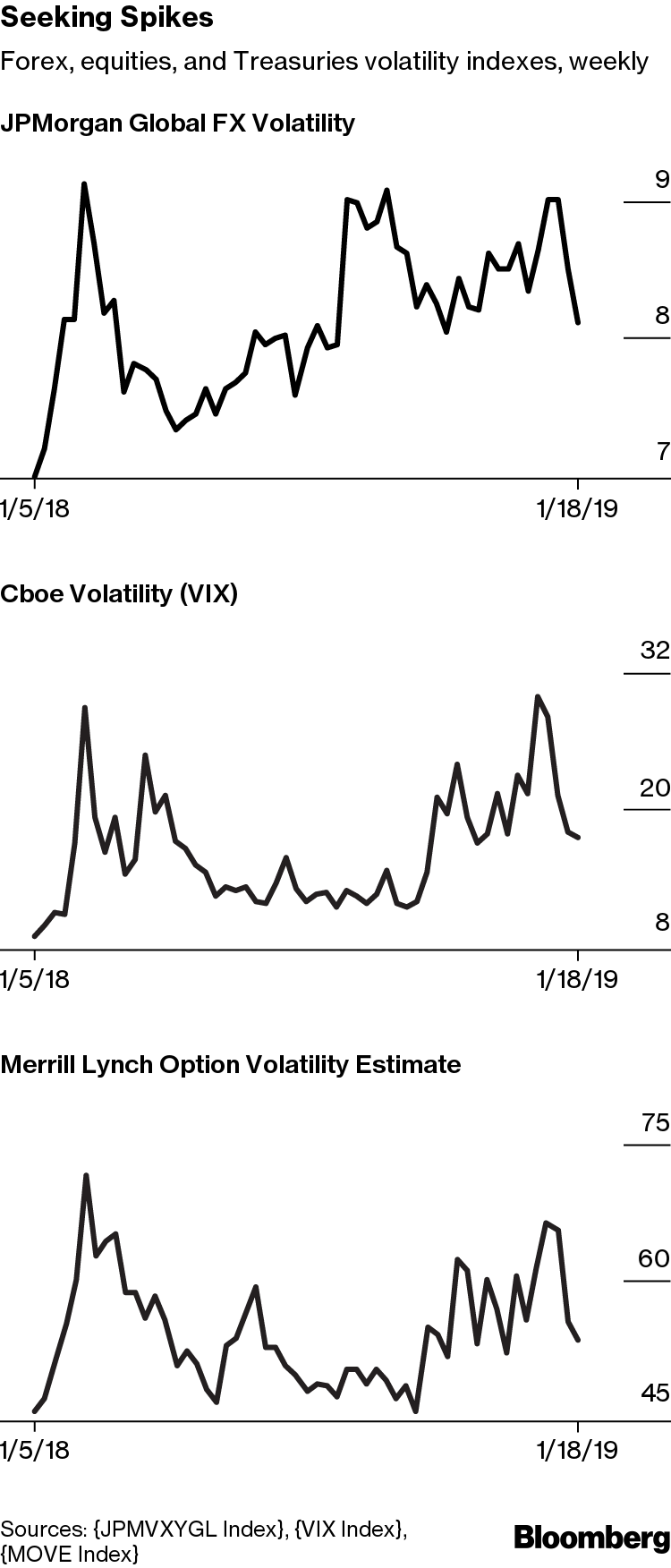

Now that it’s established in currencies and European stocks, the company is focused on expanding its U.S. footprint. Recent events may have helped. XTX said it benefited from a surge in market activity at the end of 2018 as investors became cautious about growth prospects in the U.S. and globally, driving a 9 percent slump in the S&P 500 index in December.

“One of the great things about XTX is that it was built and expanded and gained dominance in a period of lower volumes and volatility,” Swanson says. “When we do have these volatility spikes, volume increases.”